Kiddie Tax

The “Kiddie Tax” refers to a tax law in the United States aimed at preventing wealthy families from avoiding taxes by transferring investment income to their children, who typically fall into lower tax brackets. Introduced as part of the Tax Reform Act of 1986, the Kiddie Tax has undergone several amendments and remains a significant aspect of tax planning for families with substantial investment income (such as interest, dividends, etc).

Historical Background

The Kiddie Tax was first enacted in 1986 to address a loophole that allowed parents to shift income to their children, thereby taking advantage of the children’s lower tax rates. Initially, the tax applied to children under the age of 14. Over time, the age limit has been raised, and the tax provisions have been modified to close various loopholes and ensure greater tax equity.

Current Rules and Regulations

As of the latest tax law updates, the Kiddie Tax applies to the unearned income of children under the age of 19, or under the age of 24 if they are full-time students and do not provide more than half of their support. The key aspects of the Kiddie Tax are as follows:

- Unearned Income Threshold: For 2024, the first $1,300 (up from $1,250 in 2023) of a child’s unearned income is tax-free, and the next $1,3000 (also up from $1,250 in 2023) is taxed at the child’s rate, and any unearned income above $2,500 is taxed at the parent’s marginal tax rate.

- Types of Income: Unearned income includes interest, dividends, capital gains, and other investment income. It does not include earned income, such as wages or salaries from a job.

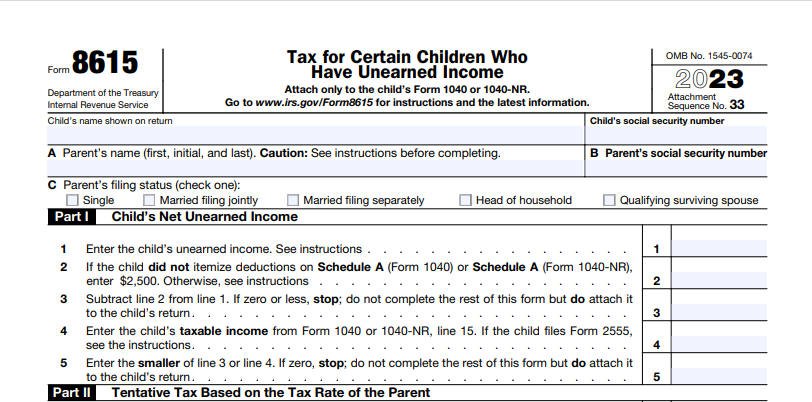

- Tax Calculation: The Kiddie Tax is calculated using IRS Form 8615, “Tax for Certain Children Who Have Unearned Income.” This form requires detailed information about the child’s income and the parents’ tax situation. A partial image of that form is below:

- Trust and Estate Income: In cases where a child receives income from a trust or estate, the Kiddie Tax rules apply, and the income is taxed at the trust or estate tax rates, which can be higher than individual rates.

Implications for Taxpayers

The Kiddie Tax has several implications for taxpayers, particularly for families with significant investment income:

- Tax Planning Strategies: Families need to consider the impact of the Kiddie Tax when planning for investments and transfers of assets. For example, gifting appreciated assets to children may result in higher tax liabilities due to the Kiddie Tax.

- Education Savings Accounts: Contributions to education savings accounts, such as 529 plans, can help minimize the impact of the Kiddie Tax by providing tax-free growth and distributions for qualified education expenses.

- Income Shifting Limitations: The Kiddie Tax effectively limits the benefits of income shifting, making it less attractive as a tax avoidance strategy. Families must explore alternative methods of tax planning that comply with current regulations.

Recent Changes and Future Considerations

The Tax Cuts and Jobs Act (TCJA) of 2017 made significant changes to the Kiddie Tax, initially tying it to the tax rates for trusts and estates. However, the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 reverted the Kiddie Tax to its pre-TCJA structure, taxing the unearned income at the parent’s rates. These legislative changes reflect ongoing adjustments to ensure the Kiddie Tax effectively targets income shifting while considering the broader impacts on families.

Conclusion

The Kiddie Tax remains an important tool in the U.S. tax system to prevent the avoidance of taxes through income shifting to children. Understanding the rules and implications of the Kiddie Tax is crucial for effective tax planning, particularly for families with significant investment income. As tax laws continue to evolve, taxpayers must stay informed about changes to ensure compliance and optimize their tax strategies.